{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.title}}

{{item.text}}

The implementation of the OECD’s Pillar Two introduces complex challenges for multinational groups with consolidated revenue over €750m. As you strive to understand the magnitude and impact of Pillar Two's 15% global minimum tax, it is important to adapt your systems, technology, processes, governance and controls to meet evolving data requirements while positioning for growth.

PwC has a tech-enabled approach, driven by the Pillar Two Engine, to help you quickly calculate the impact of Pillar Two and develop a response that is aligned to your business strategy. Supported by a global network of international tax specialists, PwC works collaboratively to develop a tailored strategy to help you assess, report and comply effectively.

A centralized, cloud-based calculation engine for quantifying the impact of Pillar Two, including provision, compliance, and modeling.

The Pillar Two Engine is adapted for relevant local rules and interpretations in order to meet Pillar Two requirements for global and statutory compliance, including constituent entity analysis, Transitional Safe Harbor assessments, and IIR, UTPR, and QDMTT computations and allocations.

Built on Beacon graph technology, the Pillar Two Engine computes accurate and visually traceable results. It is based on underlying data and uses a centralized rule library that is reviewed by global tax experts.

Learn more

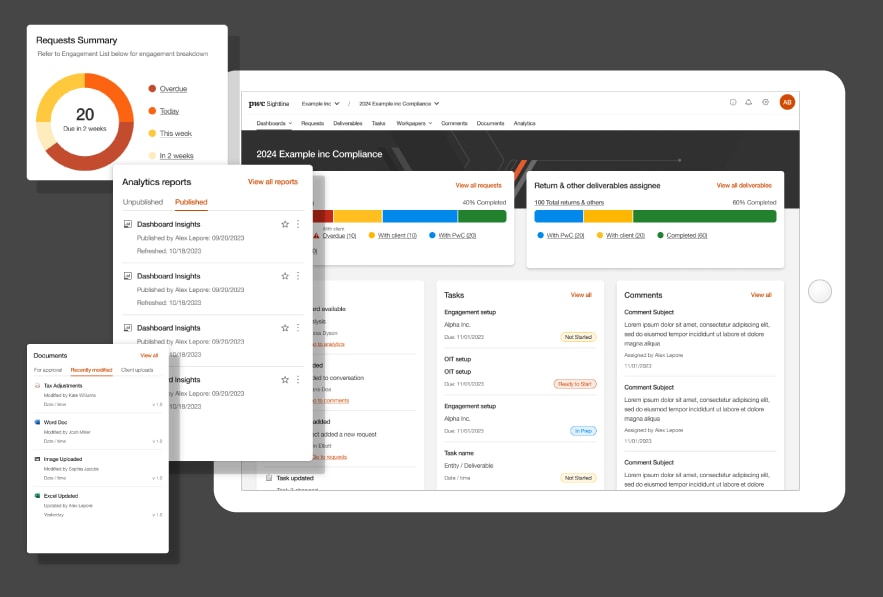

Built on the latest cloud technology with native AI integration, Sightline is your connected and intuitive tax experience at PwC. Sightline enables a true end-to-end Pillar Two experience. Starting with a dynamic questionnaire powered by our Data Input Catalog, Sightline integrates seamlessly from your systems to our Pillar Two Engine. No more manual tasks, email overload or complicated tech – take your time back and the stress out of your Pillar Two process with Sightline and our dedicated Pillar Two data and calculations specialists.

Learn more

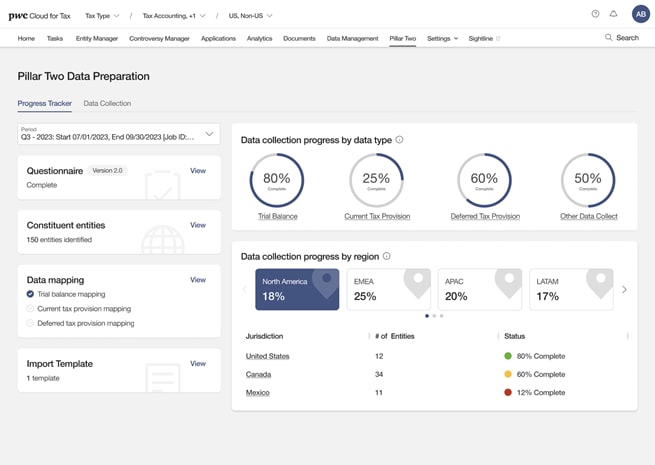

Cloud for Tax combines PwC’s tax capabilities, services, and technology experience with Microsoft’s state-of-the-art cloud solutions to help you get the most value out of your tax data and your existing technology to meet today’s complex needs. The Pillar Two module within Cloud for Tax leverages our Pillar Two Data Input catalog and dynamic questionnaire approach to assist from sourcing to staging Pillar Two data and integrates with the Pillar Two Engine.

Learn more

By leveraging our extensive Pillar Two data expertise, your existing technology infrastructure, and our comprehensive Pillar Two Data Catalog, we can help you enhance and expand the configuration of your ERP and EPM/Consolidation systems to address your Pillar Two data challenges. These systems can also be seamlessly integrated with Sightline and our Pillar Two Engine, providing a truly unified experience.

Learn more

AI is integrated into PwC’s Pillar Two process from data collection to interpreting countries’ global minimum tax laws. For example, we leverage AI for language translation and to help determine how local legislation differs from the OECD Model Rules in various countries. For data mapping and transformation, we use AI to validate that the correct source data has been acquired and where that data should map into the calculations.

Learn more